If I was going to give you a Xmas present, I'd give you some shares in FMG (Fortesque metals about 4.20 each)

because I KNOW that CEO Twiggy (Andrew Forrest) really wants to make it a success, and he has the team mentor approach will brings out the best in others. .

He is motivated. He NEEDS to win.. and he will.

So go to your banks sharebroking and invest $500-$1000.00 in FMG.

Since I don't have much money in the Kitty- I'd buy you some MHL (Monitor at .005 cents- yes at such a low price.. )

you can get 100,000 shares for your $500.00 (usually the minimum investment.)

Monitor is risky but they have no debt. They have 2 off shore rigs off WA in the Canning basin and their announcements say that they are gurgling well. They have already risen from .002 which is a 150% improvement..

PCP is another gold miner under ten cents, (My focus is on under ten cent shares) which seems to be going well, while the gold price is high... it's share price is about 10 cents and has risen by 100% over the past few months. ABY is recovering but I don't now what's happened about their un- renewed nearby tenements...

Merry Christmas and a Prosperous 2010!

from Megan

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Megamoneybox address is http://Megamoneybox.blogspot.com.au We try to help you earn money on the internet.We give free share trading tips. We aim to educate and enthuse. We are in Australia in the land of the Sun. We are asset management and risk consultants, are not financial advisors. You Trade at your own risk. We could be wrong. So do your homework. Go to our other blogs to de stress. We are not big risk takers. We asses, investigate, analyse and then decide.

Tuesday, December 8, 2009

Wednesday, October 28, 2009

ABY and Risk - MINING LEASES NOT RENEWED

I've bragged about ABY (Aditya Copper) a few times,

and this week the RISK FACTOR has been highlighted.

After battling for 18mths with a huge global downturn and rising from 11 cents to 1.60 +, ABY has been falling and badly. Why? because "the external consultants didn't renew 8 of their mining leases..adjacent to their Niffty mine". What sort of management took their eye off the ball? The mining leases are essential to their mining business !

They say that the leases were not a main part of their business, however the market is spooked and sold.

The good thing about this situation, is that although the price may drop further - because of lost confidence- shareholders can can buy back in at a lower price.

BUT IT REMINDS US, that all business, and all human endeavour (and the sharemarket) is about RISK. You must anticipate potential risk and have a plan to deal with it. The US and Australian sharemarkets are down but some companies are rising.

LKO , PDY, JRV and TAM just to name a few good resource buys under 10 cents..

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach. Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

and this week the RISK FACTOR has been highlighted.

After battling for 18mths with a huge global downturn and rising from 11 cents to 1.60 +, ABY has been falling and badly. Why? because "the external consultants didn't renew 8 of their mining leases..adjacent to their Niffty mine". What sort of management took their eye off the ball? The mining leases are essential to their mining business !

They say that the leases were not a main part of their business, however the market is spooked and sold.

The good thing about this situation, is that although the price may drop further - because of lost confidence- shareholders can can buy back in at a lower price.

BUT IT REMINDS US, that all business, and all human endeavour (and the sharemarket) is about RISK. You must anticipate potential risk and have a plan to deal with it. The US and Australian sharemarkets are down but some companies are rising.

LKO , PDY, JRV and TAM just to name a few good resource buys under 10 cents..

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach. Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Monday, October 19, 2009

tips

GDA (Gondwana gold) is rising and is now about 6 cents. I bought it at .017 cents. Many of the small resource stocks are improving, but ABY is about 1.60. Even at 1.60 it is cheap and could rise to over 4.50. (it has in the past) . goto www.asx.com.au type in ABY (or GDA etc) and have a look. Go to charts and select 5 years and you will see their charted price history.

I purchased ABY in march 09 when they were only 11 cents because this company is well managed, and has paid a dividend before.

I, like most people, regret not buying more, but the market was so volatile and at its lowest, everyone had the jitters.

I've made some modest profits lately, albeit on a very small porfolio, but "little fish are sweet" as my father used to say.

I suggest you go to http://crazyjimsmith.blospot.com and consider joining the forum.

It costs $200.00 a year, but the members post tips and information. You get access to multiple views of what's happening and if you don't go into debt, and keep your cool, you could make some profits. Then you can buy things.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

I purchased ABY in march 09 when they were only 11 cents because this company is well managed, and has paid a dividend before.

I, like most people, regret not buying more, but the market was so volatile and at its lowest, everyone had the jitters.

I've made some modest profits lately, albeit on a very small porfolio, but "little fish are sweet" as my father used to say.

I suggest you go to http://crazyjimsmith.blospot.com and consider joining the forum.

It costs $200.00 a year, but the members post tips and information. You get access to multiple views of what's happening and if you don't go into debt, and keep your cool, you could make some profits. Then you can buy things.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Sunday, October 11, 2009

ABY

Aby is still powering away now at 1.55 (I bought some in march 09 when and it had dropped to 11 cents.. still have some left from that price.

Atn is another copper explorer and up today to over .078 - nearly double . Friday it was .04 cents

there are heaps of cheapies. Buy now..

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Friday, September 18, 2009

The market is rising -- money again to pay for more things!!

I've been busy studying the market.. there are so many bargains there! Now is the time to do your research and buy a small number.

I only invest $500.00 in each company.. and that's why I try to buy well at even half a cent..

MHL is cheap and under .05 cents , PDY is on a trading halt and been rising -

QUR has risen 25% today and

ABY - my best one (it pays a dividend) which I bought at 11 cents in March, is now 1.17 and rising steadily. It has a market cap of about 265 million and I expect it to rise back to over $2.00

There are heaps of others.

Go to asx.com.au each day after 4.30 pm. go to prices /market stats/ volume risers. and find the ones in your price range. (best under ten cents) Then go to google finance, type in the code example ASX:ABY and it will come up with todays price, market cap and underneath will show other companies in the same price range and sector. It will show how they are performing. then do more homework. Then count your cents and buy for your future.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...

We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

I only invest $500.00 in each company.. and that's why I try to buy well at even half a cent..

MHL is cheap and under .05 cents , PDY is on a trading halt and been rising -

QUR has risen 25% today and

ABY - my best one (it pays a dividend) which I bought at 11 cents in March, is now 1.17 and rising steadily. It has a market cap of about 265 million and I expect it to rise back to over $2.00

There are heaps of others.

Go to asx.com.au each day after 4.30 pm. go to prices /market stats/ volume risers. and find the ones in your price range. (best under ten cents) Then go to google finance, type in the code example ASX:ABY and it will come up with todays price, market cap and underneath will show other companies in the same price range and sector. It will show how they are performing. then do more homework. Then count your cents and buy for your future.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...

We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Monday, August 10, 2009

should we invest or not?

The Australian market is rising and it seems that the recovery is on its way, however the American unemployment figures (or Australias) may not be as good as they seem. Therefore the result may not be as rosy as suggested.They may be counting part timers and casuals as "real jobs".

There may be more pain to come. BUT if you buy wisely now, you should make money in the longer term.

I bought ABY for 12 cents in April and now they are about 79 cents. Their price 12 months ago was 2.30.

I also purchased MCW for 17 cents and they are now around 56 cents. NWT is rising and at 7 cents should give a profit in the next 12 months. There are heaps of others. it's just a matter of being able to buy and hold, without using a margin loan. But it might be a rough and scary ride, so don't invest all your eggs in one basket and only buy minimal amounts.

and don't forget..I could be wrong. so do your own homework. make your own decisions. as the great guru,WarrenBuffet says, "eat your own cooking"

Mega

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

There may be more pain to come. BUT if you buy wisely now, you should make money in the longer term.

I bought ABY for 12 cents in April and now they are about 79 cents. Their price 12 months ago was 2.30.

I also purchased MCW for 17 cents and they are now around 56 cents. NWT is rising and at 7 cents should give a profit in the next 12 months. There are heaps of others. it's just a matter of being able to buy and hold, without using a margin loan. But it might be a rough and scary ride, so don't invest all your eggs in one basket and only buy minimal amounts.

and don't forget..I could be wrong. so do your own homework. make your own decisions. as the great guru,WarrenBuffet says, "eat your own cooking"

Mega

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Wednesday, July 1, 2009

Its july 1st 2009 and we've just been through the worst

2008-2009 has been probably the worst year for the share market (and superannuation funds) since the crash of 1929. Yesterday I was trying to find some shares under ten cents to alert you to..

One was PNO Pharmamet which was selling at .007 which meant you could buy 100,000 shares for about $720.00. Why PNO?- well they have, via their subsidiary company, created and patented

an over the counter arthritis medication and received a US patent on the 3.4.09.

I think it will bring good returns.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

One was PNO Pharmamet which was selling at .007 which meant you could buy 100,000 shares for about $720.00. Why PNO?- well they have, via their subsidiary company, created and patented

an over the counter arthritis medication and received a US patent on the 3.4.09.

I think it will bring good returns.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Saturday, March 14, 2009

Tip MACQUARIE COUNTRYWIDE TRUST (MCW)

todays free tip

MACQUARIE COUNTRYWIDE TRUST (MCW) is up. it was 13.5 cents on 9.3.09 and on the 15.3.09 had risen to 17.5 cents

Makes sense really.

Interest rates are down, the market seems to have bottomed, (I predicted the bottom as 19.2.09) so property is sure to rise.

if you think of the sharemarket cycle, as a circle. Then we are at the top of the circle, about to move back down the right side to a new bull market. Probably driven by property.

if you can't afford real property, then buy some property shares.

This is cheap.

The recovery could happen quickly, or may take a few months.

I think by next Xmas, we'll see a good sharemarket rise.

Mega

Disclaimer: I/we do not own any of these.. yet

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants-

we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards: AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

MACQUARIE COUNTRYWIDE TRUST (MCW) is up. it was 13.5 cents on 9.3.09 and on the 15.3.09 had risen to 17.5 cents

Makes sense really.

Interest rates are down, the market seems to have bottomed, (I predicted the bottom as 19.2.09) so property is sure to rise.

if you think of the sharemarket cycle, as a circle. Then we are at the top of the circle, about to move back down the right side to a new bull market. Probably driven by property.

if you can't afford real property, then buy some property shares.

This is cheap.

The recovery could happen quickly, or may take a few months.

I think by next Xmas, we'll see a good sharemarket rise.

Mega

Disclaimer: I/we do not own any of these.. yet

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants-

we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards: AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Wednesday, February 18, 2009

The tide has turned.. the bear is not growling!

Mega at Megamoneybox thinks the tide has turned and the recovery is on the way.

other writers say that when the recovery starts, the highest growth will be in the first 100 days, so start doing your homework.. NOW

check back to see if she was right today 19.02.2009.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

other writers say that when the recovery starts, the highest growth will be in the first 100 days, so start doing your homework.. NOW

check back to see if she was right today 19.02.2009.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Friday, February 13, 2009

free aussie stock tip by Megamoneybox

Free Aussie stock tips by Megamoneybox

Aby.ax (ADITYA FPO [ABY]) was as high as $3.00 last year, and I made 17.4% profit on sale of stock. After the stock crash it dropped to just 11 cents, then rose to 16 and now 14 cents.

This company mines copper and paid a dividend last year of 10 cents, when it was at 2.34.

I made 5 cents profit a share this week, and I am confident it will come back to at least a dollar. Check it out on the www.asx.com.au and read the announcements.

FMS- was flinders diamonds.. rising too. Check it's history on asx.

FMG Fortesque metals went down to 1.61 , but now around 2.47. Was up around $8.00 last year..

This is a time of opportunity for those who aren't greedy, and who do not risk more than they can afford to lose. DON'T BORROW TO INVEST. DON'T USE A MARGIN LOAN.

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...

We are Asset Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach. Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Sunday, January 25, 2009

Fw: A Better Way to Bailout Banks

Here something to think about.

Sent: Saturday, January 24, 2009 8:00 AM

Subject: A Better Way to Bailout Banks

Dear Colleagues:

I thought you would be interested in reading my latest essay published in the Financial Times. I critique the way it appears the government intends to spend the second tranche of TARP funding and propose an alternative.

George Soros

The Right and Wrong Way to Bail Out the Banks

By George Soros

According to reports in Washington, the Obama administration may be close to devoting as much as $100bn of the second tranche of the troubled asset relief programme funds to creating an "aggregator bank" that would remove toxic securities from the balance sheets of banks. The plan would be to leverage this amount up 10-fold, using the Federal Reserve's balance sheet, so that the banking system could be relieved of up to $1,000bn (€770bn, £726bn) worth of bad assets.

Although the details have not yet been decided, this approach harks back to the approach originally taken - but eventually abandoned - by Hank Paulson, the former US Treasury secretary. The proposal suffers from the same shortcomings: the toxic securities are, by definition, hard to value. The introduction of a significant buyer will result, not in price discovery, but in price distortion.

Moreover, the securities are not homogeneous, which means that even an auction process would leave the aggregator bank with inferior assets through adverse selection. Even with artificially inflated prices, most banks could not afford to mark their remaining portfolios to market so they would have to be given some additional relief. The most likely solution is to "ring-fence" their portfolios, with the Federal Reserve absorbing losses that extend beyond certain limits.

These measures - if enacted - would provide artificial life support for the banks at considerable expense to the taxpayer, but would not put the banks in a position to resume lending at competitive rates. The banks would need fat margins and steep yield curves for a long time to rebuild their equity.

In my view, an equity injection scheme based on realistic valuations, followed by a cut in minimum capital requirements for banks, would be much more effective in restarting the economy. The downside is that it would require significantly more than $1,000bn of new capital. It would involve a good bank/bad bank solution, where appropriate. That would heavily dilute existing shareholders and risk putting the majority of bank equity into government hands.

The hard choice facing the Obama administration is between partially nationalising the banks, or leaving them in private hands but nationalising their toxic assets. Choosing the first course would inflict great pain on a broad segment of the population - not only on bank shareholders but also on the beneficiaries of pension funds. However, it would clear the air and restart the economy.

The latter course would avoid recognising and coming to terms with the painful economic realities, but it would put the banking system into the same quandary that proved the undoing of the government sponsored enterprises (GSEs) - Fannie Mae and Freddie Mac. The public interest would dictate that the banks should resume lending on attractive terms. However, this lending would have to be enforced by government diktat because the self-interest of the banks would lead them to focus on preserving and rebuilding their own equity.

Political realities are pushing the Obama administration towards the latter course. It cannot go to Congress and ask for the authorisation to spend an additional $1,000bn on recapitalising the banks because Mr Paulson has poisoned the well in the way he demanded and then spent the money for Tarp. Even the second tranche of Tarp - the remaining $350bn - could only be pried loose by a congressional manoeuvre. That is what is leading the Obama administration to contemplate reserving up to $100bn of that tranche for the "aggregator bank" solution.

The stock market is pressing for an early decision by putting pressure on financial stocks. But the new team should avoid repeating the mistakes of the previous one and announcing a programme before it has been thoroughly thought out. The choice between the two courses is momentous; once made, it will become irreversible. It should be based on a careful evaluation of the alternatives.

President Barack Obama can fulfil his promise of a bold new approach only by establishing a discontinuity with the previous team. Congress and the public are right in feeling that too much has been done for the banks and not enough for beleaguered householders. The government ought to take the GSEs out of limbo and use them more actively to stabilise the housing market. Having done so, it could go back to Congress for authorisation to recapitalise the banking system the right way.

The writer is chairman of Soros Fund Management

Copyright The Financial Times Limited 2009

Click here to read the entire article.

More articles and essays by George Soros can be found at www.georgesoros.com

re saving tax on super

Here's some advice from smh money,

however I think if your super shares have dropped from high of 12.00 to 3.33 such as has BSL, that salary sacrificing is a waste. A 15% tax benefit, does not balance against a 70% or more loss.

Don't sell, but you should put money into something. Especially something solid and which gives a tax benefit. Like a rental property, although here beware of bank finance clauses detailing up to 20,000 dollars if you want to sell or settle early..

Oh the banks.. they caused all this and now they have free rein...

see the reference here..

David Potts

December 14, 2008

Page 1 of 2 | Single page

Page 1 of 2 | Single page

Worried about shrinking super? The tax man can ease the strain, writes David Potts.

The unlikely hero for those close to retirement whose super has shrunk is an old foe: the tax office.

It won't bring the market back to life or solve all your financial problems but, surprisingly, it can ease the pain.

"Even if you can't do anything else at least pay less tax," First State Super Financial Planning's Geoff Lawley says.

For starters salary sacrificing into super is not only the pre-eminent way of saving for retirement, it's better than ever.

True, if you'd been salary sacrificing over the past six or 12 months you'd have less super than you started with since the market has been going backwards faster than your contributions can keep up.

Pumping money into an aggressive share fund at the top of the market might have been a mistake but just as bad would be shunning it at the bottom.

Salary sacrificing stretches further in a bear market because you can afford more units in your super fund than before.

"In a sense, regular contributions are just like dollar cost averaging into the sharemarket," says executive director of Macquarie Adviser Services David Shirlow.

Remember not only is your marginal tax rate cut to 15 per cent on super contributions but if it also pulls you down the scale you'll pay less tax on everything else as well.

Admittedly while the market is weak this isn't going to make much difference to your super short term. If you were about to retire, you can't.

But there's a compromise offered by the tax system. Why not cut back your hours, which will also give you a taste of what retirement will be like?

Under the transition to retirement rules, known by various acronyms such as TRIP, TRAP and TRIS, you can draw down some of your super while still working.

It pays for itself because while there's some leakage from your super, you're still earning an income and contributing some of it back through your boss's 9 per cent contribution.

But it can be made much better by combining salary sacrificing with it.

Yep, put money in with one hand that you're taking out with the other.

A pinball-like succession of tax breaks TRIP, TRAP and TRIS their way into your super, especially if you've turned 60. On top of the stand-alone tax breaks of salary sacrificing the new ones are zero tax on your super fund (because it's moved to pension phase) and a 15 per cent rebate on the pension; or if you're 60 no tax at all.

Mega

Thursday, January 22, 2009

tips and newsletter

The gloom and doom goes on and on

but FMS Flinders diamonds

and ABY Aditya are both rising.. both earlier under ten cent stars.

I'm still an optimist and I see heaps of bargains lying on the sharemarket floor.

What I don't like is RBY Rockeby Biomed ltd, making a comsolidation just after a share offering and now my 60,000 are only 2000..... I should have sold.. the shareholders are basically funding the lifestyle of the Directors... NIo did the same last year...

a consolidation is one hting, finding your new shares trading at the same amount as before is worse... I'd rather have 60,000 at 2 cents so if they rise to 3 cents I've made a 50% profit..but right now ...it downhill all the way with RBY.

Mega

Please note that we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach. Remember you trade at your own risk. you can subscribe to our weekly newsletter and tips as they arise. The newsletter costs less than 50 cents a day or less than a cup of coffee per week....6mths fee is $190.00, one year $350.00 we will help you make money on the sharemarket.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

but FMS Flinders diamonds

and ABY Aditya are both rising.. both earlier under ten cent stars.

I'm still an optimist and I see heaps of bargains lying on the sharemarket floor.

What I don't like is RBY Rockeby Biomed ltd, making a comsolidation just after a share offering and now my 60,000 are only 2000..... I should have sold.. the shareholders are basically funding the lifestyle of the Directors... NIo did the same last year...

a consolidation is one hting, finding your new shares trading at the same amount as before is worse... I'd rather have 60,000 at 2 cents so if they rise to 3 cents I've made a 50% profit..but right now ...it downhill all the way with RBY.

Mega

Please note that we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach. Remember you trade at your own risk. you can subscribe to our weekly newsletter and tips as they arise. The newsletter costs less than 50 cents a day or less than a cup of coffee per week....6mths fee is $190.00, one year $350.00 we will help you make money on the sharemarket.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Monday, January 12, 2009

the Australian sharemarket recovery is about to

Here are a few statistics I have found which may support a far more enjoyable year for the stock market.

1. Goldman Sachs JBWere has calculated that an investor who is fully invested at a market low will on average gain 37% over the next 12 months,

whereas an investor who stays in cash for the first six months of the recovery before committing to equities for the final six months will see an average first-year return of only 6.8%.

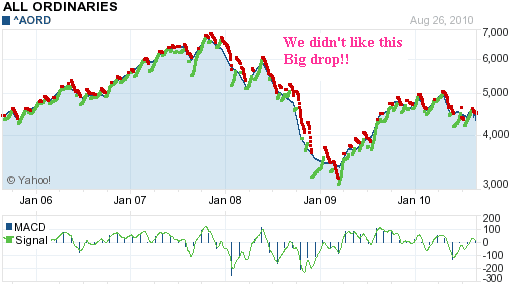

2.The All Ords has declined 19 times since 1945, and the average decline has been 14.4% (compared to a massive 45% in 2008). In the first year following a decline, the market rebounds on average by 13.5% and rebounds 80% of the time.

If the sharemarket recovery is about to happen, and current prices are at all time lows..then why wouldn't you invest ?(with a minimal amount with a considerd approach and by doing some research) This year. 2009 , presents sharemarket opportunities. you just have to look for them..

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

1. Goldman Sachs JBWere has calculated that an investor who is fully invested at a market low will on average gain 37% over the next 12 months,

whereas an investor who stays in cash for the first six months of the recovery before committing to equities for the final six months will see an average first-year return of only 6.8%.

2.The All Ords has declined 19 times since 1945, and the average decline has been 14.4% (compared to a massive 45% in 2008). In the first year following a decline, the market rebounds on average by 13.5% and rebounds 80% of the time.

If the sharemarket recovery is about to happen, and current prices are at all time lows..then why wouldn't you invest ?(with a minimal amount with a considerd approach and by doing some research) This year. 2009 , presents sharemarket opportunities. you just have to look for them..

Remember we are not financial advisors..

Sampson management Services (SMS) educate and inform only...We are Assett Management Consultants- we teach you about risk and how to measure that risk according to the international standards on Quality, Environment, OHS, and Risk management in an integrated approach.

Ref standards:

AS/NZS/ISO 9001, AS/NZS/ISO 14001, AS/NZS/ISO 4804, AS/NZS/ISO 4360.

Subscribe to:

Comments (Atom)